Worldwide Semiconductor Revenue in 2023 Declines by 11.1%

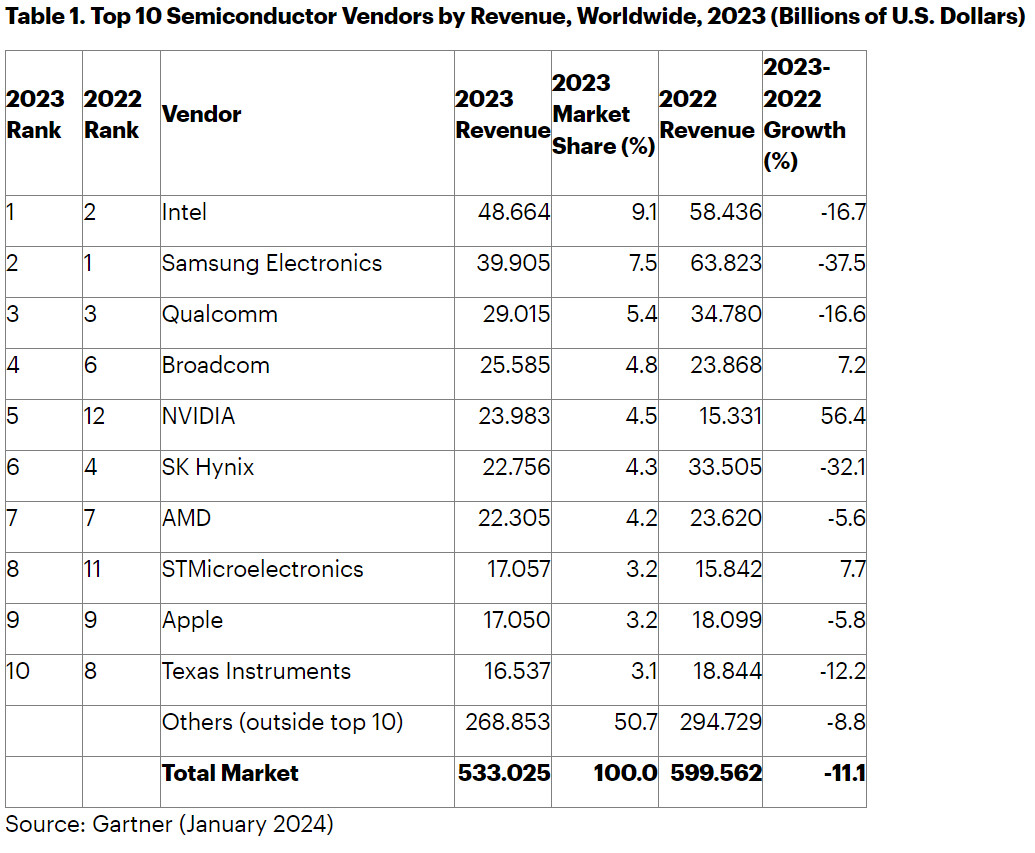

According to preliminary results by Gartner, Inc., worldwide semiconductor revenue in 2023 reached $533 billion, marking an 11.1% decrease from the previous year.

"While the semiconductor industry experienced its usual cyclical nature in 2023, the market faced significant challenges with memory revenue recording one of its worst declines in history," said Alan Priestley, VP Analyst at Gartner. "This underperformance also had a negative impact on several semiconductor vendors, with only 9 out of the top 25 vendors seeing revenue growth in 2023, while 10 experienced double-digit declines."

The combined semiconductor revenue of the top 25 vendors declined by 14.1% in 2023, accounting for 74.4% of the market, down from 77.2% in 2022. In terms of rankings, Intel regained the No. 1 spot in 2023, surpassing Samsung after two years in the No. 2 position. Intel's revenue for 2023 totaled $48.7 billion, while Samsung's revenue reached $39.9 billion. Nvidia also made significant progress, with its semiconductor revenue growing by 56.4% to reach $24 billion, placing the company in the top five for the first time ever. This growth can be attributed to Nvidia's leading position in the artificial intelligence (AI) silicon market. STMicroelectronics also moved up three spots to secure the No. 8 position, driven by a 7.7% increase in revenue, primarily in the automotive segment.

Memory products experienced the largest decline in revenue, with a 37% decrease in 2023. "Smartphones, PCs, and servers, which are major segments for DRAM and NAND, faced weaker demand and excess channel inventory, particularly in the first half of 2023," explained Joe Unsworth, VP Analyst at Gartner. DRAM revenue declined by 38.5% to reach $48.4 billion, while NAND flash revenue decreased by 37.5% to $36.2 billion.

On the other hand, nonmemory revenue declined by 3% in 2023. The segment was affected by weaker demand and excess channel inventory throughout the year. However, unlike memory vendors, most non-memory vendors experienced a relatively stable pricing environment. The demand for non-memory semiconductors for AI applications was the strongest growth driver, with the automotive sector, especially electric vehicles, as well as the defense and aerospace industries, outperforming other application segments.

Gartner clients can find more information in the report "Market Share Analysis: Semiconductors, Worldwide, 2023 (Preliminary)."